AARP Eye Center

New Thinking about Budgeting for Your Second Adulthood

By Heather Nawrocki, July 15, 2013 02:53 PM

This is a guest post by Bart Astor.

For years financial planners have been preaching that in your retirement years you should plan on spending about 70% of your current income. This number was based on a number of factors, including:

- You don't need to continue to save for your retirement years

- You won't be paying into Federal Insurance Contributions Act Tax (Social Security and Medicare)

- You won't have commuting and work expenses

- Your house will be close to or already paid off.

To me, this is old-world thinking for the following reasons:

- You need to continue to save for your later years because you will likely have 20, 30 or more years left

- A third of folks in their 60's continue to work or have encore careers and still pay into FICA

- Even if you stop or cut down on your work, you'll still have travel expenses

- Fewer and fewer homeowners ever pay their mortgages off completely, plus many people rent, not own.

So given the fact that living on the magic 70% was based on outdated reasoning, what number should we use when planning our budgets? My estimate is 81.3%. How did I come up with that number? Simple, really. I took the original recommended 70%, added back in half of what we ought to be saving now for your retirement years (half of 10%), added back in half of the FICA, presuming that we will work about half time (half of 7.65%), added back in half the current commuter/travel expense (half of 5%), and discounted totally the mortgage or rent reduction.

That brings us to the 70% plus 11.325%, or 81.3% of your current income. Now mind you, I did not factor in additional medical expenses which, as we know, generally increase as we get older. But since we become eligible for Medicare at 65, it's possible that some people will pay less for medical care and medical insurance than what they're paying now. Just to be safe, I'd round the 81.3% up a bit, to 82%.

Bottom line: when planning for your second adulthood and retirement years, use 82% of your current income as your best estimate of how much you'll need to live on.

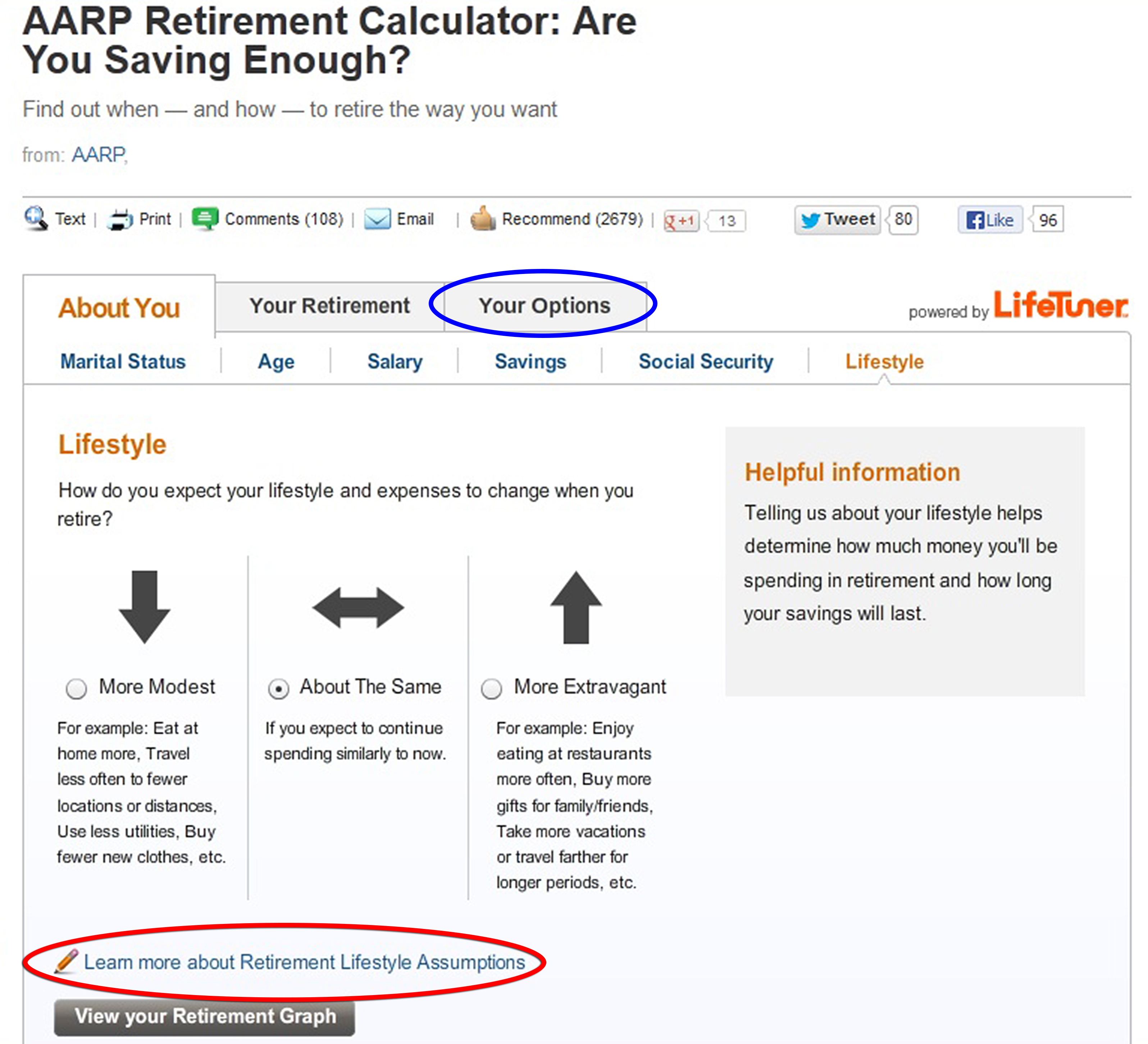

For a more customized figure, the AARP Retirement Calculator helps you figure out how much income you'll have - and how much more you might need - in retirement. Under "Lifestyle," the tool asks you whether you plan to live a more or less extravagant lifestyle in retirement. On that page, you can click "Learn More About Retirement Lifestyle Assumptions" to set an assumption (e.g., 82%) that's more appropriate for you. You can get even more precise by clicking on the "Your Options" tab and then click "Adjust Lifestyle" to input your own retirement expenses [as shown below].

About the author: Bart Astor is a recognized expert in life's transitions and eldercare. In addition to AARP Roadmap for the Rest of Your Life: Smart Choices about Money, Health, Work, Lifestyle, and Pursuing Your Dreams, Bart wrote the best-selling book, Baby Boomer's Guide to Caring for Aging Parents, and has appeared on numerous TV and radio shows, including ABC's "Good Morning America," PBS's "MarketPlace," AARP Radio, and Ric Edelman's "The Truth About Money." | Photo credit: Eli Meir Kaplan

Retirement sign photo credit via Flickr Creative Commons: 401(K) 2012