AARP Eye Center

Are You an Irrational Investor? Here's How to Tell

By Allan Roth, November 17, 2014 10:48 AM

Too many of us are irrational investors. Acceptance of this fact and understanding the roots of our irrationality are the keys to better investing.

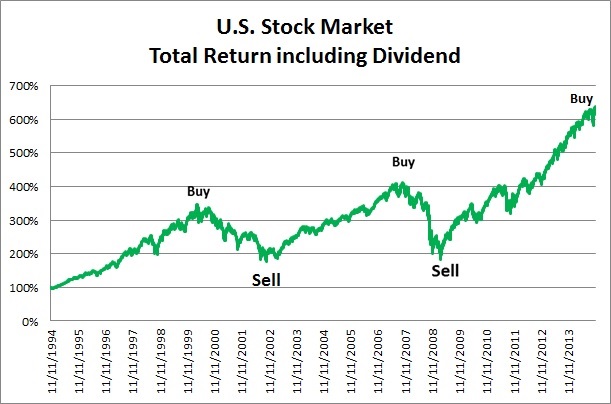

First, the facts. Many studies show that a lot of investor money moves in and out of stock funds at the wrong time, often buying high and selling low. For example, at the height of the 2007 stock market bubble, investors were pouring money into stock mutual funds. After the 2008 plunge, however, those same investors took their money out of stock funds and ran for the hills, not to return until 2013, when stocks were hitting an all-time high.

>> 5 Bad Investment Moves to Avoid

This cycle of performance chasing is almost as regularly repeated and predictable as the phases of the moon. Data from Chicago-based Morningstar illustrates that over the past 10 years, investors timed their activity so poorly that their performance lagged the average fund by nearly 2.5 percentage points annually. Carl Richards, an author and adviser, calls it the behavior gap.

Why we are irrational

Behavioral finance holds the key. It is a relatively new field that seeks to combine behavioral and cognitive psychological theory with conventional economics and finance to provide explanations for why people make irrational financial decisions.

I teach behavioral finance to financial planners, CPAs and attorneys. As part of the class, I ask them to describe what money means to them. I get words like the following:

- freedom

- security

- choices

- enjoyment

To me, money represents stored energy that powers our dreams for the future. Money may not buy happiness, but the stored energy it provides gives us the freedom to pursue happiness.

With this understanding, back in 2007, with stocks at an all-time high, our stored energy was growing and that freedom was ever closer. So we selectively ignored any warning of a bear stock market and bought the argument that real estate could never decline. We shifted our portfolio more heavily toward stocks in order to reach independence even sooner.

But after the 2008-09 plunge, we saw our stored energy decrease dramatically, and the number of years we had to work to recoup our losses increased. Would we end up spending our golden years on the clock rather than pursuing our retirement dreams? We bought the predictions of a great depression ahead hook, line and sinker. “Cash is king” was uttered by so many experts that sheer desperation drove us to sell at the bottom. Even last month, with an 8 percent decline in stocks, some investors believed it was the world’s end and panicked.

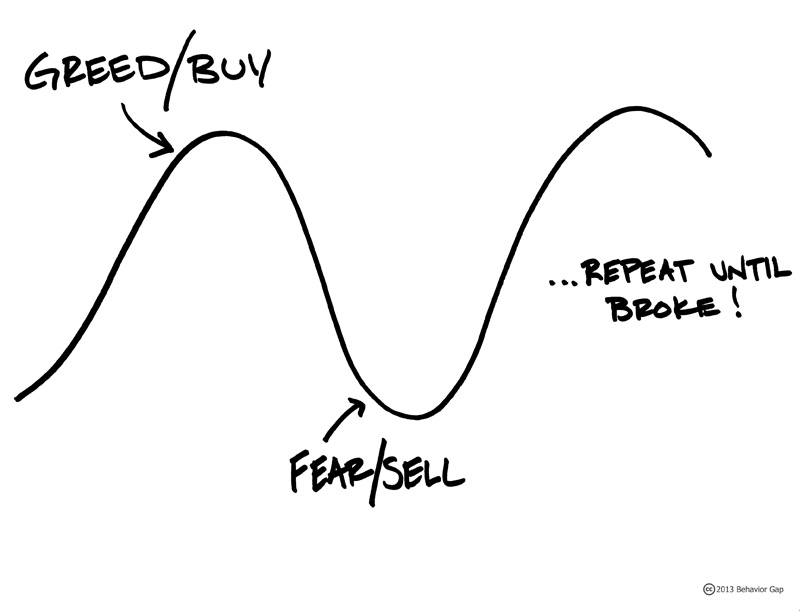

That is but one example of the age-old cycle of fear and greed. The instincts that fuel this cycle are likely what kept us alive as a species but, unfortunately, they fail us when it comes to investing.

Pain is the key to good investing

Looking back at the first 15 years of this century, buying stocks at the half-off sale generated by the bursting of the tech and real estate bubbles was a painful process. I tell clients it was like being kicked in the gut three times and asking for three more. Selling stocks then felt oh-so-good as it made the pain stop, but it ultimately locked in the losses.

To a lesser extent, it also hurt to sell stocks at the height of both bubbles, but that was also the right thing to do. The pleasure of buying more stocks would only lead to disaster.

>> Get discounts on financial services with your AARP Member Advantages.

What this means to you today

Markets are near an all-time high and it’s predictably irrational that money is continuing to move into stocks. Clearly, we don’t know if stocks will plunge or surge next year, but we do know that neither good nor bad times last forever.

So if you pick an allocation percentage in stocks, and commit to stick with it, you are likely to do better. For some, this means selling some stocks now (yes, that’s painful) to get back to that allocation.

Chart Data: Wealth Logic VTSMX - data from Yahoo Finance

Also of Interest

- Why Insurance and Investing Often Don’t Mix

- What's the Maximum Social Security Benefit?

- Get Involved: Learn How You Can Give Back

- Join AARP: savings, resources and news for your well-being

See the AARP home page for deals, savings tips, trivia and more.