AARP Eye Center

Are Longevity Annuities in Your Future?

By Allan Roth, February 18, 2015 09:00 AM

I’ve been pretty critical of many annuities in the past, but there is one out there that might be worth a serious look. It’s called a Qualified Longevity Annuity Contract (QLAC) — yes, that’s a mouthful. Recent technical changes to this annuity OK’d by the U.S. Treasury offer a partial solution to the not-outliving-your-money challenge.

Unlike many other annuities, this one is fairly straightforward and easy to understand. It also has some tax advantages. In fact, in five years, says Stan Haithcock, aka Stan the Annuity Man, the QLAC will be the No. 1 owned annuity in America. Haithcock wrote about this recently and explained how the QLAC works.

So what is it? A QLAC is a type of deferred annuity in which you pay the insurance company today in exchange for a monthly check for the rest of your life, starting sometime in the future. You can put as much as 25 percent of your IRA savings (up to a maximum of $125,000) into a QLAC. You then select whatever age you want the monthly check to begin, as long as it’s no later than 85.

A tax benefit of the QLAC is that those funds are not subject to required minimum distributions from your traditional IRA that normally start after age 70½. This allows you to further delay paying taxes on part of your IRA savings. The monthly checks are typically taxed as ordinary income, assuming all of your IRA funds were contributed on a pretax basis.

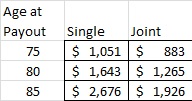

Using a QLAC

Let’s look at an example of how a QLAC could be used. Irwin is 65 years old with a $400,000 IRA. He wants to enjoy his money but, like many of us, he’s afraid of running out of cash. And while statistically speaking he has a life expectancy of 83, he is healthy and his family genes suggest there’s a good chance he’ll live well beyond age 85 and possibly even beyond 95.

So if Irwin put $100,000 into a QLAC, he could buy a monthly check of $2,676, beginning at age 85, according to Haithcock. This would allow Irwin greater peace of mind to spend more of his remaining portfolio, now that he knows he would receive this regular check to partially offset his living expenses later. This particular policy also would allow Irwin’s heirs to receive the $100,000 if he died before age 85.

If Irwin wanted to receive the monthly checks sooner, or if he was married (spouse also age 65) and wanted the checks to continue while either is alive, the amount would be less, as shown on this table with quotes provided by Haithcock. He could also buy an inflation-adjusted annuity that would pay less, with the inflation adjustment beginning when he started collecting the checks.

My Analysis

This type of annuity is a very efficient form of longevity insurance, and the tax break makes it even more attractive. It could even be used to pay for long-term care costs, thus decreasing the need to buy long-term care insurance.

>> Get discounts on financial services with your AARP Member Advantages.

To my mind, though, delaying Social Security is still the best longevity insurance out there. Why? Because it’s like buying an inflation-adjusted annuity at a 45 percent discount. In other words, if you consider the monthly checks you could have received as a premium for larger checks later, it’s a much better deal than you could buy on the open market.

QLACs are relatively simple and easy to understand — and that’s also a huge plus. I find that simple and transparent financial products are nearly always superior to complex products. So the QLAC could be appropriate for part of your nest egg.

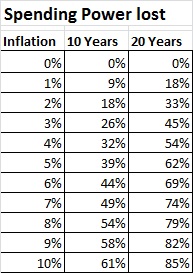

The big drawback I see is that, so far, no insurance company has offered a deferred annuity (QLAC or otherwise) that protects against inflation between the time the annuity is purchased and when the checks begin. Inflation is very hard to predict. If, for example, inflation averages 2 percent (the Fed target), then only 33 percent of the spending power would be lost in 20 years. If, however, we have 5 percent annual inflation, then a full 62 percent of spending power is gone and the check will not go very far. Perhaps that offering will come soon.

Photo: olm2650/istock

Also of Interest

- Should I Buy Long-Term Care Insurance?

- Want to Drop Pounds Fast? Try These Tactics

- AARP Foundation Tax-Aide: Get free help preparing and filing your taxes

- Join AARP: savings, resources and news for your well-being

See the AARP home page for deals, savings tips, trivia and more.