AARP Eye Center

Under the Senate Health Bill, All Older Adults Would Pay Much More for Individual Health Coverage

By Lina Walker, Jane Sung, Claire Noel-Miller and Olivia Dean, June 27, 2017 01:39 PM

The just-released Senate bill, the Better Care Reconciliation Act (BCRA), is very bad news for older adults. The bill would reduce financial assistance (premium tax credits and cost-sharing subsidies) and change rules on how much premiums can vary by age (age rating). As a result, people ages 50 to 64 would have to pay thousands of dollars more in premiums to buy health insurance in the individual (nongroup) market.

Here are four ways the bill would increase the cost of health insurance for adults ages 50-64:

#1: Older adults would pay five times more than other adults.

The bill would allow insurers to charge people 50 and older up to five times more than younger adults (as opposed to up to three times more under current law) — known as 5:1 age rating. We estimate that this change alone would increase older adults’ premiums by over $4,000 a year on average across all states.¹

But the bill does even more to make coverage unaffordable.

#2: Many older adults would no longer qualify for premium assistance and would have to pay significantly more.

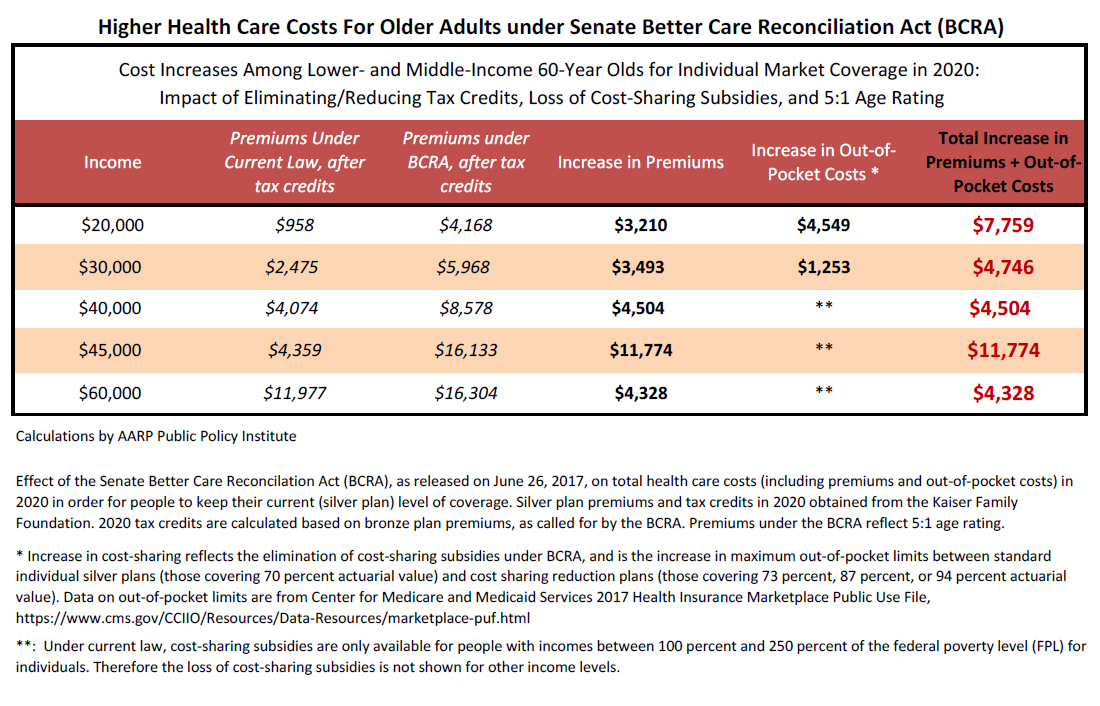

Starting in 2020, the bill would eliminate premium tax credits for people who earn between 350 percent and 400 percent of the federal poverty level (FPL), which corresponds to incomes between $42,210 and $48,420 in 2017.

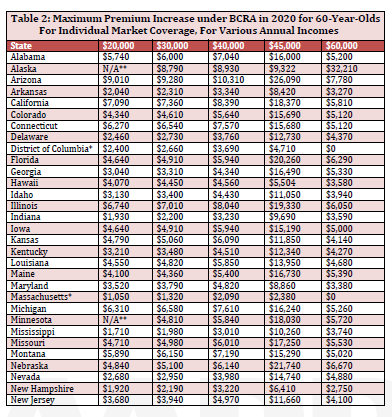

When the bill is in effect, a 60-year-old earning $45,000 would have to pay $11,800 more a year in premiums than under current law just to keep the same level of coverage he or she has today (Table 1). The premium under BCRA would be $16,133 a year — over a third of that $45,000 annual income, and more than 3½ times what they would pay under current law. The impact of this change would be even worse in some states, especially in rural areas and parts of the country where health care costs are high (see Table 2 for premium increases in all states). In West Virginia, for instance, that same 60-year-old would end up paying up to $22,530 a year, which is nearly $18,200 more than what they would under current law. In Alaska, a 60-year-old who loses eligibility for this assistance would pay up to $38,300 a year for the same coverage — a whopping $32,200 more a year than under current law.

#3: Older adults eligible for premium assistance would receive much less financial help.

The BCRA would significantly reduce premium tax credits for people who still qualify for financial assistance; consequently, millions of older adults would pay a lot more under the bill. Current law protects people with lower and moderate incomes by capping their premium payments. The Senate bill would increase the cap for older people and require them to contribute more of their income. In addition, under current law, the amount by which a person’s premiums are reduced (the tax credit) is based on the price of a silver plan. Under the Senate bill, tax credits would be based on the price of a bronze plan. Don’t be fooled by the technical nature of this change — it has huge implications. Since bronze plans costs less (because they cover less) than silver plans, this means that tax credits under the BCRA would be far smaller than under current law.

As a result, even those qualifying for tax credits would face higher premiums. A 60-year-old earning $40,000 would have to pay $4,500 more in 2020, — an increase from $4,000 under current law to over $8,500 — just to keep the same level of coverage.

#4: Older adults with lower incomes would no longer receive critical cost-sharing reductions to afford their care.

And finally, the bill would eliminate subsidies that nearly 70 percent of 50-to-64-year-olds with premium tax credits receive. These subsidies, known as federal cost-sharing reductions, are available to people with incomes at or below $31,250 a year. They help them pay for out-of-pocket costs like deductibles, coinsurance and copays. Eliminating these cost-sharing reductions means that a person earning $20,000 a year could face up to $4,500 more in out-of-pocket bills. This increase would be in addition to the increase in premiums they would face!

Here is the bottom line: Under the Senate’s Better Care Reconciliation Act, all older adults would face significantly higher costs for individual coverage.

¹Calculations by AARP Public Policy Institute, based on premium data from the Kaiser Family Foundation. Estimated premium increases are for 2020 if people keep their current silver level of coverage.

Click here to download Table 1

Click here to download Table 2

Michael JN Bowles

Michael JN Bowles

Lina Walker is vice president at the AARP Public Policy Institute, working on health care issues.

Claire Noel-Miller is a senior strategic policy adviser for the AARP Public Policy Institute, where she provides expertise in quantitative research methods applied to a variety of health policy issues related to older adults.

Jane Sung is a senior strategic policy adviser with AARP’s Public Policy Institute, where she focuses on health insurance coverage among adults age 50 and older, private health insurance market reforms, retiree coverage, Medicare supplemental insurance and Medicare Advantage.

Olivia Dean is a policy analyst with the AARP Public Policy Institute. Her work focuses on a wide variety of health-related issues, with an emphasis on public health, health disparities, and healthy behavior.

Search AARP Blogs

Recent Posts