AARP Hearing Center

Credit Reporting Change on Low-Balance Medical Debt is a Positive Step Forward, Benefitting Many Older Adults

By Kyra Brown, James McSpadden, January 22, 2025 10:49 AM

In a recent AARP focus group, Malcolm (name changed for privacy), a 64-year-old man with health insurance through his employer and a preexisting condition, shared how over the course of a year, he received two low-balance medical bills he couldn’t afford to pay. The bills went to collection, which elevated his stress, and, in turn, caused his health to deteriorate. That meant additional care, which resulted in more bills and, ultimately, more medical debt. He found himself in a vicious cycle from which he is still trying to escape.

Many older adults like Malcolm carry low-balance medical debt—under $500—that is sold to collection agencies. According to an AARP analysis of 2022 Survey of Income and Program Participation (SIPP) data, more than 2.5 million adults ages 50 and older had medical debt under $500 that were sent to collection and ultimately reported on consumer credit reports. Among the medical collections that appeared on consumer credit reports between 2017 and 2022, 34 percent of those carried by adults ages 45 to 61 and 15 percent of those carried by adults ages 62 and older totaled less than $500.

In April 2023, the three major credit rating bureaus (Equifax, Transunion, and Experian) voluntarily began to eliminate medical debts of less than $500 that are sent to collections from all consumer credit reports, as well as removing reports of medical debts that were already paid. This historic change had a favorable benefit for many consumers, including adults ages 50 and older, leading to improved credit scores and lowering the cost of borrowing.

Recently, federal regulators finalized a rule to eliminate all medical debt from credit reports. These changes recognize that medical debts are unique and often unpredictable debts, and that non-payment of medical debts is not predictive of one’s willingness or ability to pay back credit voluntarily borrowed. Even so, state and federal agencies should adopt additional policies to lessen the burden that medical debt poses for many older adults.

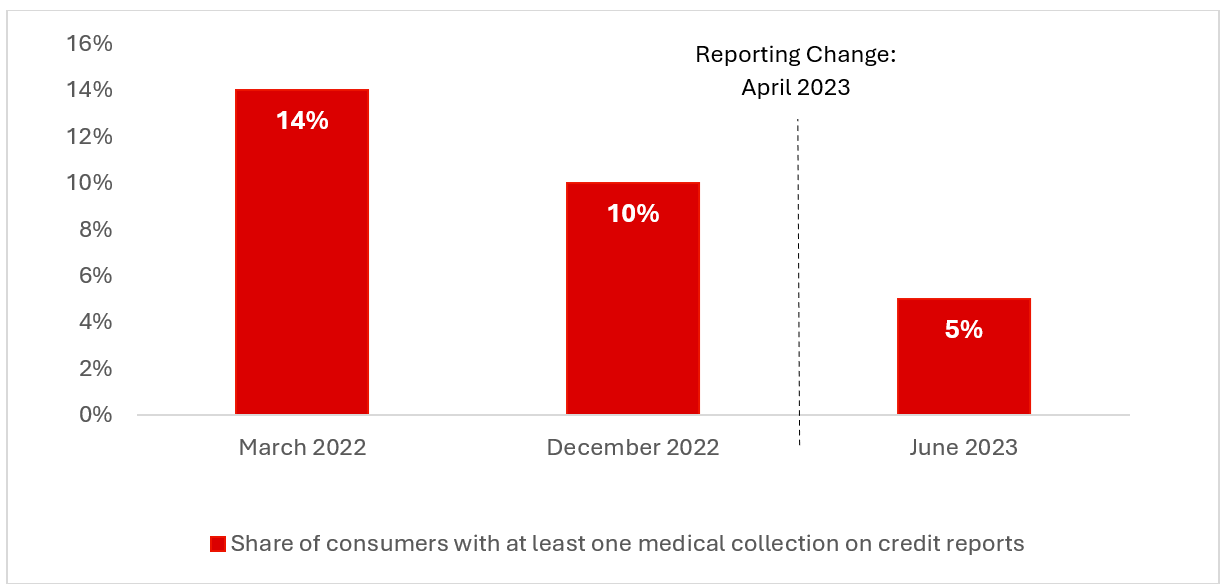

Positive change: fewer older adults have medical collections on credit reports

When the credit bureaus removed low-balance medical collections, the number of consumers with observed medical collections on their credit reports dropped dramatically. A Consumer Financial Protection Bureau (CFPB) analysis of a sample of five million credit records showed that 60 percent fewer consumers had medical collections on credit reports in June 2023 as they did in March 2022. Additionally, the sample showed that the percentage of consumers with medical collections on their credit record dropped from around 14 percent in March 2022 to 5 percent in June 2023, and he average number of reported medical collections per consumer dropped from 2.5 to about 1.7 in the same period. As such, CFPB estimates that 15.6 million adults still had a medical collection remaining on their credit reports in June 2023.

After Voluntary Agency Reporting Change, The Share of Consumers With Medical Collections on Credit Reports Between December 2022 and June 2023 Dropped by Half

Note: Prior to the voluntary agency reporting change to eliminate medical debts of less than $500 that are sent to collections from all consumer credit reports, medical collections had started to fall for a variety of reasons including a voluntary change by the three major reporting bureaus in July 2022 to exclude paid medical debt on a consumer’s credit report and extend the period before unpaid medical debt appeared on a credit report from six months to one year.

Many of the consumers whose collections were removed from reports were older adults. Despite 92 percent of midlife adults having health insurance coverage, CFPB sample data showed that 16 percent of adults ages 45 to 61 had medical collections on their credit reports. That share fell to 7 percent after the voluntary reporting change. The share of adults ages 62 and older with medical collections on credit reports was 8 percent in March 2022, a smaller share than midlife adults due, in part, to many in this age group having Medicare coverage. This figure fell by more than two-thirds to 3 percent after the reporting change. The acuteness of the drop in both age groups may reflect the high number of low-balance medical collections due to higher rates of chronic conditions and billing complexity resulting from a person having multiple providers and health insurance plans (e.g., Medicare and Medicaid).

Reporting change may improve older adult’s financial health

Medical debt is unique in that it is a type of debt consumers do not voluntarily take on, unlike a mortgage or a car loan. Medical debt is also not a good predictor of creditworthiness; in fact, consumers with medical debts on their credit report repaid debts at the same rates as consumers whose credit scores were approximately 20 points higher. However, the presence of medical debt collections on credit reports has lowered credit scores. Fortunately, a significant result of the reporting change has been improved credit scores. An Urban Institute report found that the average credit score of consumers whose medical debt collections disappeared from credit reports increased from 585 (August 2022) to 615 (August 2023).

Individuals with higher credit scores as a result of the change can enjoy increased financial security and expanded access to credit products with lower interest rates and higher returns on investment. They can, for example, more easily rent an apartment, get approved for a car loan, purchase home insurance, and increase their financial borrowing capacity. Higher credit scores are especially important for older adults who might need to open new lines of credit to cover basic needs like out-of-pocket health care costs or caregiver-related expenses.

Reporting change is a first step

While the credit agency reporting change has meaningful benefits, debt collections and medical debt remain issues for older adults.

The voluntary reporting change only eliminated low-balance collections from credit reports. As such, many older adults continue to have larger medical debt collections on their credit reports. After the reporting change, the CFPB observed that among adults with medical collections on credit reports nearly a third (31 percent) were ages 45 to 61 and 15 percent were adults 62 and older.

Moreover, the source of the issue remains. Regardless of what a credit report shows, many older adults are dealing with medical debt. Close to half of adults ages 50 to 64 and more than one in five adults ages 65 and older report carrying some level of medical debt, ranging from hundreds of dollars to over $10,000. 2022 SIPP data showed that more than 8.6 million adults ages 50 and older had medical debt on credit reports that exceeded $500; 40 percent had debt exceeding $5,000; and 10 percent exceeding $25,000.

Such debt can affect both financial and physical health. For example, 62 percent of Medicare-age adults with health care debt reported delaying, skipping, or seeking alternatives to needed health care or prescription medications in the past year due to costs. Also, higher levels of debt are found to increase stress, resulting in increased likelihoods of medical conditions. With respect to financial health, debt during retirement may reduce asset accumulations and result in lower levels of retirement income security.

Medical debt, collections, and credit reports moving forward

The voluntary reporting change is a significant step forward for adults ages 50 and older. Removing low-balance medical debt collections from credit reports will not only benefit large numbers of older adults who had been unfairly penalized for having medical conditions that may not be fully covered by insurance, but will also provide a fairer reflection of the likelihood that consumers will pay other debts that they may have willingly incurred. Put simply, removing low-balance medical collections from credit reports improves credit scores, which in turn may improve the health and financial well-being of this population. Recently, the CFPB has issued a final rule to ban the inclusion of all medical debt on credit reports and limit the use of medical collections by creditors. AARP submitted comments in support of this rule, though others are challenging the rule in court.

Policymakers should attend to the effects that existing, larger-balance medical debt collections currently have on older adults’ credit and find ways to help relieve the medical debt burden carried by so many older adults. Additionally, policymakers should consider future debt accumulation—as adults ages 50 and older remain particularly vulnerable to acquiring medical debt due to chronic conditions and insurance billing complexities and inaccuracies. Further steps are needed to directly address the affordability of health care, so that fewer people have to face the problems of medical debt, medical collections, and the resulting repercussions.

Search AARP Blogs

Recent Posts