AARP Hearing Center

Payroll Deduction Savings Programs Improve Retirement Security: State Auto IRAs are Vital to Expanding Coverage

By David John, Manita Rao, Gary Koenig, December 12, 2024 11:11 AM

New AARP research finds that about half of American working adults, or about 56 million people, lack access to a payroll-deduction workplace retirement savings plan, making it much more difficult for them to save for retirement. Small business employees, workers with low-to-moderate earnings, and Black and Hispanic workers are especially at risk. Fortunately, some states are leading the way to close this coverage gap through innovative policy solutions that are now available.

The research results are based on an AARP analysis of Census data using a groundbreaking methodology published by The Wharton School of the University of Pennsylvania and developed by a former Federal Reserve expert to provide the most accurate estimates of who does not have access to a workplace retirement plan.

Why is access to a workplace retirement savings plan so important for retirement security? Because employees are 15 times more likely to save for retirement if they have access to a payroll deduction savings plan at work. Retirement savings success comes from consistently saving small amounts over a long period of time. Investment returns help those amounts to grow, eventually producing enough to supplement a person’s Social Security benefits. Without payroll deduction savings plans, and the features that often accompany these benefits, such as automatic enrollment, people rarely save enough regardless of their best intentions.

The national retirement coverage gap

The retirement coverage gap spans across all workers, regardless of earnings or employer size, but it is most prominent among small employers and workers with low- and moderate-earnings. About 78 percent of workers in firms with less than 10 employees, 64 percent in firms with between 10 and 24 employees and 34 percent in firms with more than 1,000 employees do not have access to a way to save for retirement through the workplace. Further, over 44 million workers who have annual earnings of $53,000 or less and another 12 million workers with earnings of more than $53,000 cannot save for retirement through a workplace plan.

The retirement coverage gap is also higher among women, Hispanic and Black workers. About 48 percent of women do not have access to a workplace retirement plan compared to 46 percent of men. Nearly 63 percent of Hispanic workers, 52 percent of Black workers, and 44 percent of Asian American workers lack access to a workplace retirement plan. In addition, three out of four workers with less than a high school degree, 50 percent of workers with some college and 31 percent of those with a bachelors’ degree do not have access to a retirement savings plan. Finally, close to 40 percent of workers over age 45 and nearly 56 percent of adults between ages 18 and 34 lack access to a workplace plan.

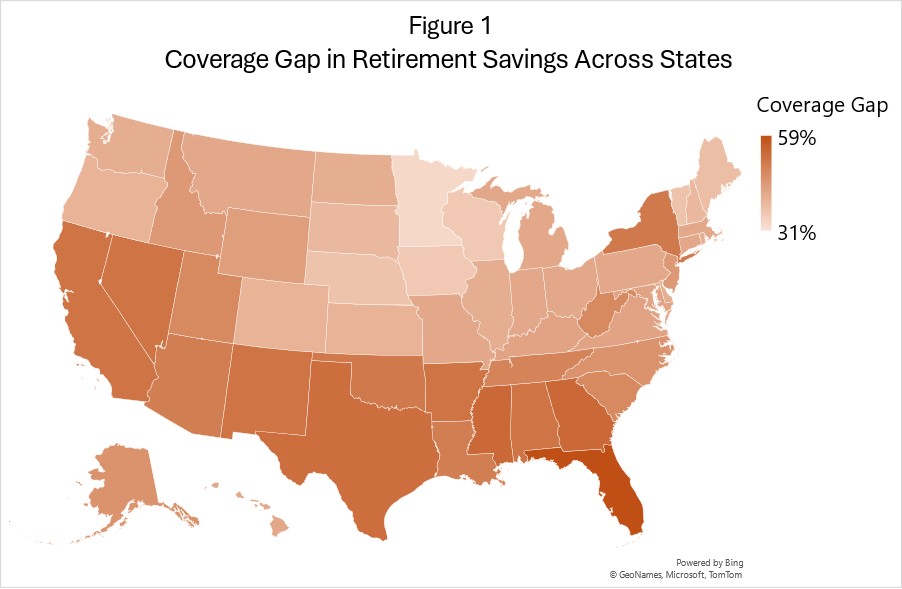

Differences in retirement plan coverage across states

AARP research, which examined data from all 50 states and the District of Columbia individually, shows that access to workplace retirement savings programs also differs across individual states (see map below). Among individual states, between 31 percent and 60 percent of workers lack the ability to save for retirement at work. Florida has the highest proportion of its workforce without a retirement savings program, while the District of Columbia has the lowest.

In addition to Florida, states with over half of all workers lacking coverage include Arizona (50.3 percent), New York (51 percent), Oklahoma (51.3 percent), Alabama (51.6 percent), Arizona (51.8 percent), California (52.1 percent), Nevada (52.2 percent), New Mexico (52.3 percent), Texas (53.4 percent), Georgia (54.1 percent), and Mississippi (54.1 percent).

At the opposite end of the spectrum, Minnesota, Wisconsin, and the District of Columbia have the lowest percentage of workers who are not covered by a retirement savings plan. Across these three jurisdictions, between 30 and 36 percent of workers lack access to such a benefit.

State Auto IRA and similar programs provide a path forward

The absence of an easy and seamless way to save for retirement makes building retirement security difficult. Ideally, every American should have the ability to save for retirement through a payroll-deduction workplace retirement savings plan from the day they begin working until the day they retire. One way to accomplish this would be to require employers to offer some type of retirement savings program. Although the topic has been debated and several bills have been introduced in recent years, Congress has yet to act.

Meanwhile, several states have already taken steps to close the retirement savings coverage gap. Those states require employers to offer a retirement savings program to workers through a privately provided plan (e.g., 401(k)) or a state-facilitated and privately managed option, typically structured as an automatic enrollment Individual Retirement Account (Auto IRA).

The first of these states to act was Oregon, which in 2017 started OregonSaves, a state-facilitated, privately managed option for workers to save for retirement through payroll deduction. The structure is somewhat similar to the existing Section 529 college savings accounts offered in just about every state. The following year, both Illinois Secure Choice and California’s CalSavers began to accept savings from employees working in those states, and then other states followed suit. As of December 2024, 13 states have expanded access to workplace retirement savings plans through Auto IRA or similar programs and seven additional states are in the process of implementing programs. As of October 2024, workers have saved over $1.75 billion in 933,000 accounts, and that number is growing rapidly as new state programs open.

Most states use the Auto IRA because it offers a highly effective, simple, and low-cost retirement savings option. There are no fees or requirements on employers other than that they automatically enroll employees and send their payroll contributions to the system. Employees have full control over their savings, but unless they decide not to participate, they are enrolled in the program and save a set amount in a specific investment option. If they wish, workers can save more or less than the default amount and choose a different investment type.

Employers can choose to offer their own 401(k)-type benefit instead of participating in the state-facilitated program and many have chosen to do so. Among the early-adopter states (CA, OR, IL, and CT), over 30,000 employers have chosen the private plan option, either initially or once they had some experience with retirement savings benefits through the state program. And all employers benefit from being able to attract and keep better employees because they can offer a retirement program.

Conclusion

The retirement security for roughly 56 million workers can be significantly improved by increasing access to payroll deduction retirement savings accounts. Doing so would especially benefit low-to-moderate income workers, and employees of small- and mid-sized businesses.

While Social Security remains the bedrock of American retirement security, almost all workers will need additional resources to supplement that income and provide money for unexpected expenses. This challenge can be addressed by requiring all employers to offer their workers a retirement benefit of some type.

Learn more by reading the national fact sheet and state fact sheets.

Search AARP Blogs

Recent Posts