AARP Hearing Center

State Auto IRA Programs Spur Expansion in Private-Plan Market

By Manita Rao, February 12, 2025 10:24 AM

Access to an employer-based, payroll-deduction retirement savings plan plays a key role in allowing people to save for the future. Yet nearly half of American workers, or about 56 million, do not have access to such a plan. To address this challenge, in recent years a growing number of states have passed legislation requiring employers to offer their employees a workplace, retirement savings plan either through a privately provided plan, such as a 401(k), or a state-facilitated Auto IRA program. Access to payroll deduction retirement accounts provides workers an easy and simple way to put money aside for their long-term financial security.

Data on state-facilitated Auto IRAs demonstrate that these programs have been a success. As of December 2024, about a million workers have saved nearly $2 billion dollars in these state-facilitated savings programs. New research I co-authored finds that states that were early adopters of Auto IRA policies witnessed faster growth in private retirement plans than states without Auto IRA policies. More than 30,000 companies in early-adopter states chose to start new private plans to help employees save for retirement in the workplace. This study adds to a growing body of research showing that state Auto IRA policies are having a positive impact on the private market for retirement plans, such as 401(k) accounts, laying to rest fears that these policies might cause a shift away from private retirement plans and toward the state-facilitated option.

Research findings

The research, which I co-authored with Adam Bloomfield,[i] Lucas Goodman,[ii] and Sita Slavov,[iii] finds that since the inception of these state programs, many small- and mid-sized firms have adopted retirement plans. Moreover, in addition to the new retirement programs offered through the state option, these state policies have driven an expansion of privately provided plans. This positive consequence is another force helping to achieve the legislation’s core purpose of improving retirement security for all American workers. Both the Auto IRA programs themselves and new private retirement savings plans have helped reduce the coverage gap.

Our research study investigated the impact of state retirement savings requirements on the private retirement market by examining 11 years of data covering 2012 through 2023 and using advanced econometric methods. It sheds light on the response of employers to Auto IRA legislation in the first four states — California, Oregon, Illinois, and Connecticut — that implemented state-facilitated retirement savings programs.

Employers in states that first passed Auto IRA legislation saw a substantial growth in the adoption of private workplace retirement plans. We found that over 30,000 employers in the early-adopter states chose to set up a private plan rather than to use the state-facilitated option. This effect is significant since establishing and maintaining a private plan is typically more costly than the state-facilitated option, although private plans such as 401(k)s have certain advantages (e.g., higher employer contribution limits). Furthermore, our analysis shows that the increase in private retirement plans is largely the same regardless of firm size.

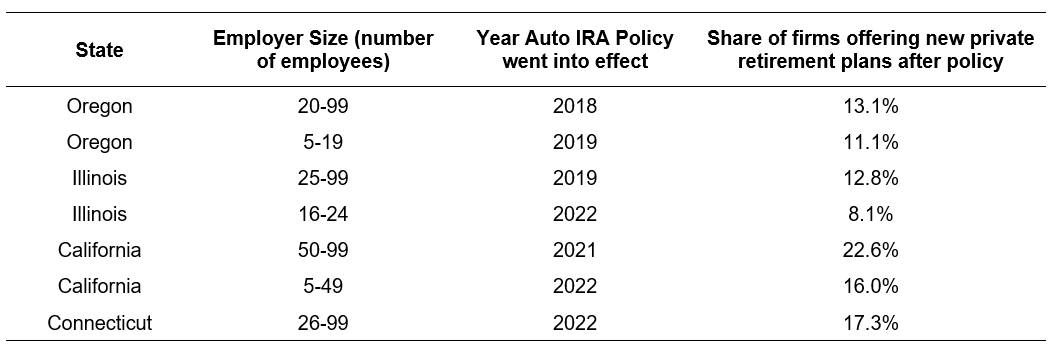

The table below shows the percentage of employers by state and number of employees (employer size) that chose to start a new private retirement plan after each state’s Auto IRA policy went into effect. Auto IRA policies were phased in over time by employer size, starting with larger firms and moving to the smaller ones, and each state had different categories of small and mid-sized employers. The share of employers that started offering new private retirement plans after the policy came into effect ranges from 8 percent for small firms (16 and 24 employees) in Illinois to 23 percent among mid-sized firms (50 and 99 employees) in California.

Percentage of Employers that Started a Private Retirement Plan

What about employers that already had private plans?

In addition to the number of employers choosing private plans in response to the new policy, there is also the question of how the policy has impacted employers that already had private plans in place. In theory, the introduction of a low-cost option[iv] like the state-facilitated Auto IRA program might lead some employers to shift away from their current higher-cost private plan in favor of the state option. However, we found no evidence of this. Although some individual employers might have shifted to the state option, the net effect was an increase in the adoption of private plans. It is worth noting that private retirement service providers may also have responded to Auto IRA laws by introducing lower-cost options, thereby aiding in the overall expansion of the retirement plan market.

The policy takeaway

Retirement savings are critical to the long-term financial well-being of individuals and households. Access to simple and affordable ways to save for retirement is a pre-requisite to achieve long-term financial goals. Our research shows several employers responded to state Auto IRA policies requiring them to offer a retirement benefit by establishing new workplace retirement plans like a 401(k)-type plan from private sector providers and other employers responded by choosing to enroll employees in the lower-cost state-facilitated retirement savings program. These results are an indication of the Auto IRA policy’s success in expanding the private retirement plan market and helping employees make progress toward achieving their retirement savings goals.

_________________________________________________________________________________

[i] Senior Economist, FDIC

[ii] Financial Economist, Office of Tax Analysis, The Department of Treasury

[iii] Professor, School of Public Policy, George Mason University and Non-Resident Scholar, American Enterprise Institute

[iv] Previous research shows that retirement plan costs are a barrier for small and mid-sized employers. To address this concern, states that enacted Auto IRA legislation created a simple, low-cost state-facilitated option for employers that did not choose to offer a private sector retirement plan. These Auto IRA programs are available at no cost to employers and area easy and affordable for their workers. (For survey research on retirement plan concerns of small and mid-sized firms, see: https://crr.bc.edu/wp-content/uploads/2023/10/2023-Small-Business-Survey-Report.pdf)

Search AARP Blogs

Recent Posts