AARP Hearing Center

Warning: Short-Term Health Plans = Higher Premiums for Older Adults

By Jane E. Sung , March 21, 2018 12:05 PM

You might have thought that efforts to unravel the Affordable Care Act (ACA) were over, but newly proposed regulations and legislation are once again threatening to have similar harmful effects for older adults ages 50-64 who rely on individual market coverage.

On February 21, 2018, the Trump Administration proposed new federal rules calling for significant expansion of a category of insurance products known as “short-term limited duration” insurance plans. More recently, Congress is considering legislation that would block states, who typically regulate these plans, from taking steps to protect consumers from the harms of these proposed federal rules once they are finalized.

Unfortunately, these changes would result in much higher premiums for older adults and people with preexisting health conditions buying individual policies through the ACA Marketplace.

What are Short-Term Limited Duration Plans?

Short-term limited duration plans, or short-term plans, have long been available for sale. Carefully regulated to prevent abuse, short-term coverage may be appropriate for specific circumstances, such as when people are in between jobs or need brief periods of coverage and don’t qualify for special enrollment into more comprehensive coverage.

Short-term plans, however, are extremely limited in many ways. They are exempt from many important ACA consumer protections, such as protections for people with preexisting conditions. They typically require medical underwriting, which means that only healthy people can qualify to purchase them. Short-term plans do not have to cover essential benefits, such as prescription drugs or mental health, and can impose annual and lifetime limits on coverage. As such, short-term plans are usually offered at a low premium.

Under current rules, short-term plans are only available for three months and cannot be renewed beyond that – making them truly for “short-term” needs. These federal limits were put in place in 2016 to protect consumers in response to reports that short-term plans were being abused by insurance companies.

Troubling Changes Proposed

Under the new federal proposed rules, however, short-term plans would see a dramatic expansion. Instead of the current three month limit, insurance companies would be allowed to provide coverage under the plans for up to 364 days, and possibly longer. This change effectively makes them almost identical in duration to plans that are required to comply with the ACA.

This change, along with Congress’ recent elimination of the ACA’s requirement that people have health insurance that provides minimum essential coverage (known as the individual mandate), means that we are now likely to see many more plans called “short-term” plans even though they run for up to a full year.

Short-Term Plans will not Protect Older Adults and People with Preexisting Conditions

Proponents of expanded short-term plans tout them as a more affordable health insurance option. In reality these plans will fall well short of properly serving older adults and people with preexisting conditions. To start, the ability under these plans to deny coverage for preexisting conditions is especially troubling because 40 percent of people ages 50-64 have a pre-existing condition. Short-term plans are not required to comply with ACA age rating protections so insurance companies could charge older adults more than three times the premium they charge other people, or even deny them coverage based on age.

Moreover, while short-term plans may initially seem attractive for their low cost, they are unlikely to protect consumers when they need insurance most since they lack coverage of essential benefits and key ACA consumer protections.

Expansion of Short-Term Plans will drive up premiums in the individual health insurance market

Even worse, the expansion of these plans will increase premiums for everyone, including older adults and people with preexisting conditions, who remain in the individual health insurance market. Short-term plans, with their skimpy coverage and lower price, are likely to siphon off healthier people from the market. This means that older people and those with greater health needs who remain in the individual health insurance market will have to pay more for their coverage. This is especially troubling for older adults, who already pay higher premiums than other age groups and who will see larger dollar increases.

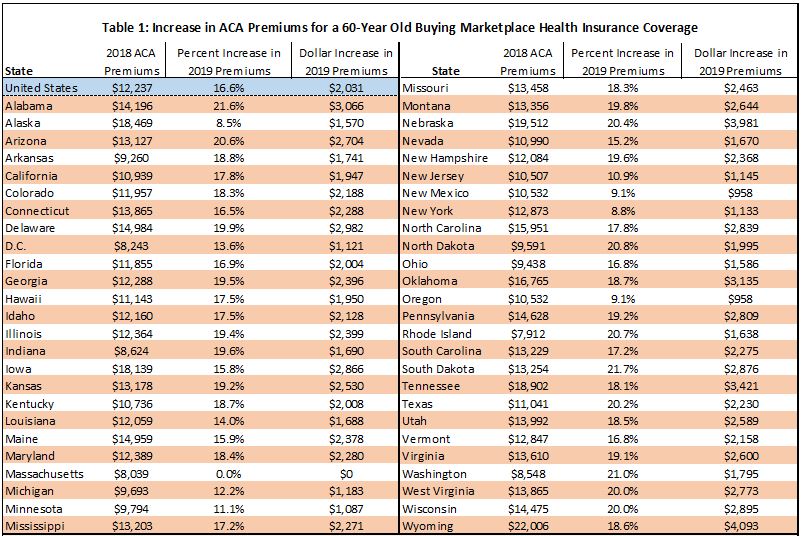

The Urban Institute estimates that the proposed regulatory changes, in combination with the repeal of the requirement to have minimum essential health insurance coverage, will increase premiums by an average of 16.6 percent in 2019 -- even as high as 22 percent in some states.

Using 2018 Marketplace premiums, we estimate these premium increases could be an average of $2,000 -- or as much as $4,000 (Table 1) -- for 60 year-olds who buy silver plan coverage. Premium increases would be even higher than shown for six states (Massachusetts, Michigan, Nevada, New Jersey, New York, and Oregon) under the proposed legislation, since it would prevent states from adopting rules to protect consumers.

In sum, expansion of short-term plans are a troubling development in the effort to maintain affordable health coverage for older adults and people with preexisting conditions.

Table 1 - Increase in ACA Premiums

Notes: Premiums based on second-lowest cost silver (benchmark) premium for a 60-year-old buying in the Marketplace. Premium increase from expansion of short-term limited duration plans as specified in February 21 2018 Health and Human Services Proposed Rules and from repeal of the federal requirement for health insurance coverage.

Source: Kaiser Family Foundation analysis of 2018 data from Healthcare.gov, state rate review websites, and state plan finder tools at: http://kaiserf.am/2DI5Eif. CMS Healthcare.gov data on 2018 federal exchange plans at http://bit.ly/2DJGorJ. Urban Institute's analysis of impact of short-term duration plans on ACA Marketplace premiums at http://urbn.is/2G07k8E.

Jane Sung is a senior strategic policy adviser with AARP Public Policy Institute, where she focuses on health insurance coverage among adults age 50 and older, private health insurance market reforms, Medicare Advantage, Medigap, and employer and retiree health coverage.

Lina Walker is vice president at the AARP Public Policy Institute, working on health care issues.

Search AARP Blogs

Recent Posts