AARP Hearing Center

Essential yet Elusive: Inflationary Pressures Underscore Urgency for Emergency Savings Policies

By Manita Rao, December 13, 2022 10:20 AM

This blog is first in a new series on ‘Savings and the Economy’. The series provides data-driven insights on the implications of economic instability for household savings and discussions on policies that enable financial wellbeing.

The US economy is in the midst of one of the worst inflationary periods in recent history. After a four-decade hiatus, inflationary concerns are today widespread. In the weeks leading up to the midterms, Americans viewed inflation as the top problem facing the nation, 80% were concerned that inflation and overall economic instability will affect their financial wellbeing. Inflation has touched nearly every aspect of household spending, the rise in prices of everyday goods and services such as food, energy, utilities, and housing have implications for the ability of families to weather financial emergencies. Amid the economic turbulence that American families are facing, policies that will help families save for financial emergencies, while essential to financial wellbeing, remain elusive.

Trends in Inflation and Household Savings

Inflation refers to an economic phenomenon which measures the rate at which prices increase over a period of time. The past four decades were a period of stable and low inflation in the US, conditions that aid economic growth and better enable families to build financial wealth. The economic uncertainty that inflation causes affects the hiring and wage decisions of firms, and routine household decisions. When prices of groceries, medicine, the cost of healthcare, and rents change frequently, households are required to factor in the higher volatility that stems from fluctuating macroeconomic conditions into their spending and savings decisions.

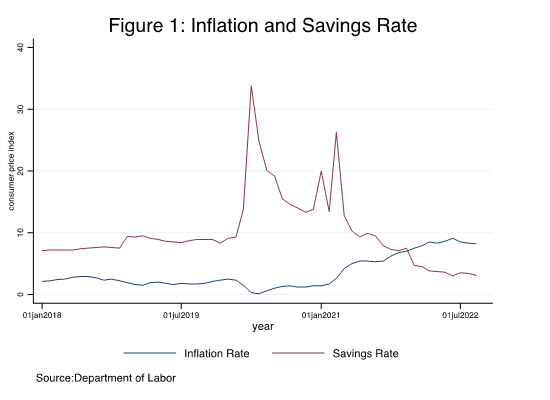

Figure 1 shows trends in inflation (the Consumer Price Index) and household savings between early 2018 and late 2022. The Consumer Price Index (CPI), the blue line in the figure, is the indicator of inflation, it measures monthly price changes of goods and services consumed by a typical family. It is evident that price pressures have increased substantially over the past four years. Price inflation which began in mid-2021 has escalated quickly since March 2022 and was highest - 9.1% - in June 2022. The good news is that even though inflationary pressures remain elevated, well above the federal reserve’s benchmark 2% inflation rate, inflationary pressures have slowed in recent months. In October, inflation dropped by 1.4 percentage points to 7.7%, a welcome relief for many American families.

Household savings, however, have declined sharply over the past few months after reaching an all-time high of 33% in April 2020 [footnote 1]. The household savings rate is the share of disposable income that families save to meet their short- and long-term needs. The drop in household savings is concerning because families with savings are better prepared to weather unexpected financial emergencies, especially for older adults on fixed incomes and low-and moderate-income households. Even before the pandemic, 44% of households did not have emergency or rainy-day fund to cover financial emergencies and nearly half indicated the need to borrow money or sell assets to cover a $400 emergency expense. High inflation imposes further pressure on the ability to save, a critical aspect of preserving financial wellbeing.

Policy makers have an opportunity to help families build emergency savings by supporting policies that advance workplace emergency savings. Over half of US workers do not have access to retirement savings through their workplace, increasing the likelihood they will not be financially secure in their retirement. Apart from retirement savings, but equally concerning is that even fewer workers have access to workplace emergency savings. Policies that reduce regulatory barriers and enable automatic enrollment will help expand access to workplace emergency savings programs. Harnessing the power of automatic enrollment with payroll deductions is vital to helping American families achieve greater retirement security. The added benefit of workplace savings programs is that such approaches alleviate the higher costs that families incur in searching for financial products and services that meet their near-term savings needs. By reducing such search costs, families with access to workplace emergency savings will improve their financial security.

There continues to be a need to better enable families to save, both for the near and long term. For the near term, increasing access to emergency savings programs not only helps strengthen the ability of families to meet emergency and unplanned expenses, it also can help reduce the likelihood of tapping into retirement savings early to meet immediate needs. In the long term, programs to increase retirement savings can greatly enhance an individuals’ ability to retire securely.

Emergency savings are essential to enable American families achieve financial security. Although policies that further workplace emergency savings have remained elusive, unexpected inflationary pressures and the ensuing economic instability highlight importance of workplace emergency savings policies to help Americans achieve a secure retirement.

[1] The high savings rate in early 2020 resulted from host of factors including COVID lockdowns, stay-at-home mandates, shuttering of businesses during the pandemic, and federal relief payments provided by the governments to reduce the economic burden of pandemic related layoffs on families. With few avenues to spend, families were able to accumulate savings and strengthen their financial positions. This high rate should be treated as an anomaly, the pre-pandemic average household savings rate is 7%.

Search AARP Blogs

Recent Posts