AARP Hearing Center

If You Get Health Insurance From Your Job, the Health Care Debate’s Outcome Could Still Hurt You

By Lina Walker and Jane Sung, May 25, 2017 11:24 AM

Getty Images/iStockphoto

People with health insurance through large employers may assume the outcome of the current health debate won’t affect them. But it can. To start, yesterday the Congressional Budget Office (CBO) estimated that 3 million people would lose employer-based insurance coverage as a result of changes proposed in the American Health Care Act (AHCA). But the bill’s harmful effects would reach far beyond those 3 million people; in fact, virtually everyone is vulnerable. Here’s how:

In times of change, people turn to the individual market.

Even if you’re one of the fortunate 39 million 50- to 64-year-olds currently receiving health insurance coverage through their employers, that may not always be the case. You may lose your job, need to quit for health reasons, choose to retire early, or decide to start your own business. Or perhaps someone you know will divorce or become widowed, and lose coverage they had through a working spouse. These situations can happen to anyone. While COBRA coverage may be available, it can be expensive and only available for a limited time. Thus, people in these situations turn to the individual health insurance market.

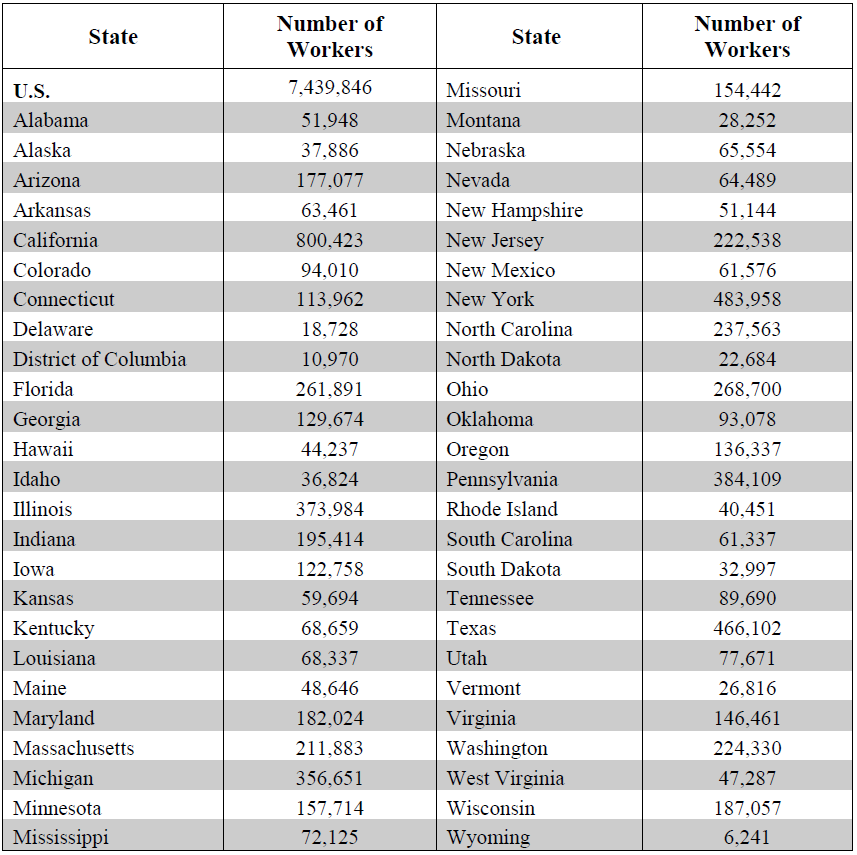

How often do these type of changes happen? Quite often, actually. According to government data every year, about 7.4 million Americans who work for a large employer experience a break in employment lasting four or more weeks. Whatever the reason for the break in employment, it could leave them without insurance. The numbers vary by state, and in large states, such as California, it can be over 800,000 people. (See table below.)

Older adults could get hit in several ways.

Older adults who have to leave coverage through large employers and turn to the individual market would face the brunt of the harmful changes being proposed by the health bill. These changes include allowing insurance companies to charge older adults five times or more what others pay for the same coverage, significant reductions in tax credit assistance that helps people pay for coverage, and allowing discrimination against people with preexisting conditions.

Because of these and other harmful changes to the individual market, older adults would be prevented from retiring early or from being able to start their own business.

But the people with job-based coverage are in the clear, right? Not so fast.

People who remain in job-based coverage will still be affected, because the health bill weakens current rules that protect workers enrolled in coverage through large employers. These rules ensure that coverage is affordable by requiring insurance companies to limit consumers’ annual out-of-pocket spending (such as deductibles, copays and coinsurance) and prohibiting insurance companies from setting lifetime and annual limits on coverage that could put them at risk of medical bankruptcy.

Bottom line: No one can afford to ignore the debate on the health bill.

Number of Working Adults in Large Firms with a Break in Employment of Four Weeks or Longer, Who Might Seek Coverage in the Individual Market

Source: AARP Public Policy Institute

Lina Walker is vice president at the AARP Public Policy Institute, working on health care issues.

Jane Sung is a senior strategic policy adviser with AARP’s Public Policy Institute, where she focuses on health insurance coverage among adults age 50 and older, private health insurance market reforms, retiree coverage, Medicare supplement insurance and Medicare Advantage.

Notes: Urban Institute tabulations from the 2008-2013 Panel Survey of Income and Program Participation data, pooled for years 2010-2012. We thank Karen E. Smith and Aaron Williams at the Urban Institute for the tabulations. A break in wage and salary employment includes (1) job loss for any reason, (2) early retirement or (3) leaving paid salary work for self-employment, within a 12-month period. Large firms are those with 50 or more employees. Includes workers ages 18-64.

Search AARP Blogs

Recent Posts