AARP Hearing Center

Inflation Hits Home Care, Increasing Pressure on Older Adults and Family Caregivers

By Brendan Flinn, October 15, 2024 09:43 AM

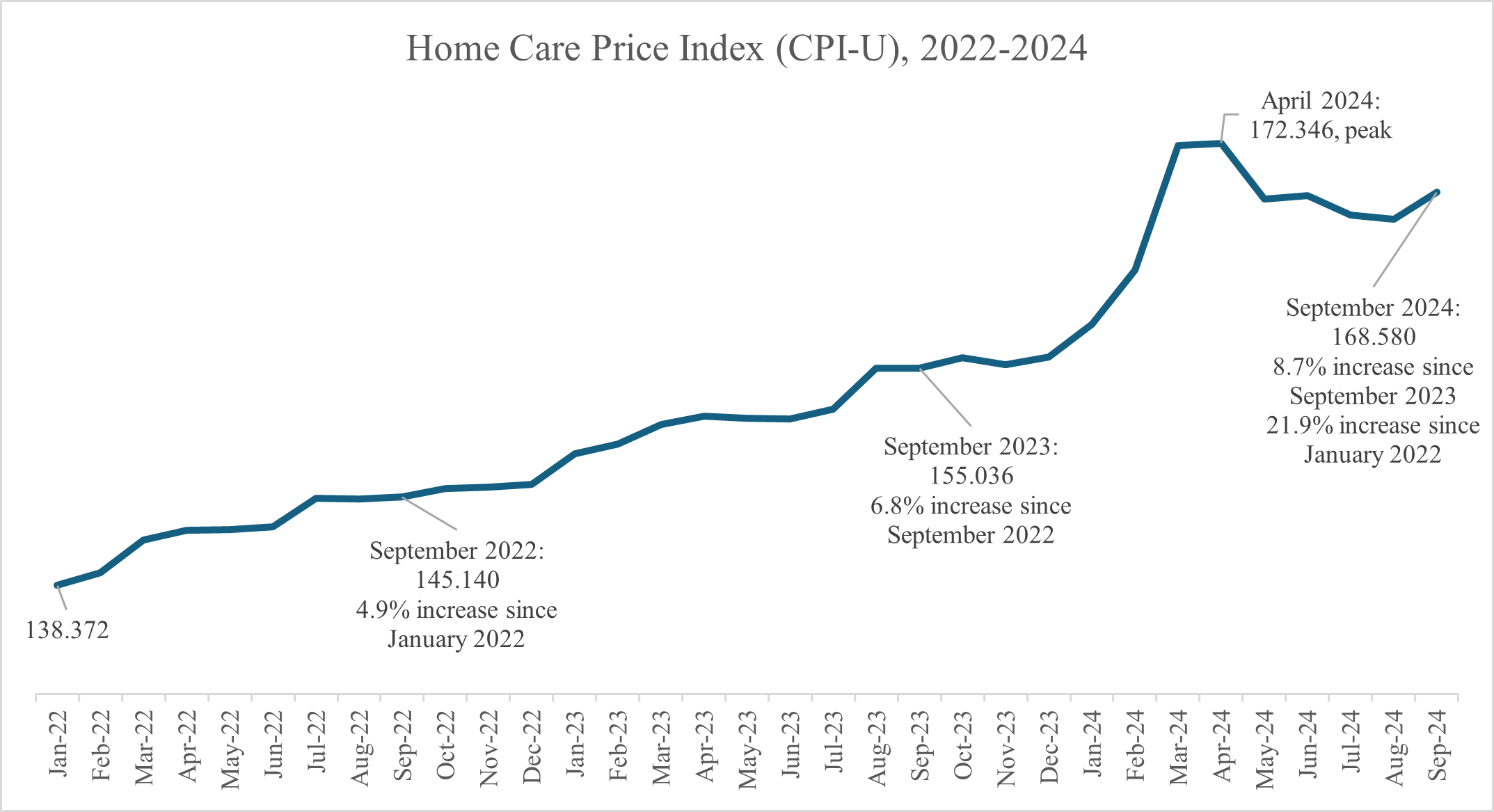

In recent years, American households have faced challenges from inflation, with prices surging for much of 2021 and 2022. And inflation has not solely impacted trips to the grocery store or the gas station. Spikes in the cost of home care that outpace even general inflation present specific and unprecedented difficulty for older adults, people with disabilities, and family caregivers. In June 2022, the most recent inflation peak, prices generally rose by 9% year over year but have slowed down significantly since then. From September 2023 to September 2024, general inflation increased by just 2.4% while home care inflation rose by 8.7%.

At a median hourly cost of $30 per hour in 2023, or more than $60,000 annually for full-time care, home care is already prohibitively expensive for many household budgets and often in high demand. High home care inflation will only further increase pressures on individuals and families that need this support.

Costly, pervasive need

About half of older adults at some point in their lifetimes will need long-term services and supports (LTSS), such as help with day-to-day tasks that support people with functional limitations and/or cognitive impairments. The reality, however, is that paid LTSS is unaffordable for most families. High inflation for home care and other LTSS will only increase and hasten the impact on those needing paid care.

Earlier this year, an AARP Public Policy Institute analysis found that the median annual cost of care for most LTSS exceeded both the median assets and household income of older adults. In other words, the need for care is often out of reach and can be financially devastating for many households. Well-documented disparities both in income and assets only increase the pressures home care inflation may place on older Black, Hispanic, and Native Americans.

Most older adults live on fixed and often modest incomes, with limited budgets that cannot sustain rapid cost increases. As a result, they may face one of various scenarios: going without the care they need, relying more heavily on family caregivers to provide more unpaid care or drawing from savings to pay for care and more quickly “spending down” their assets to the point of becoming eligible for Medicaid.

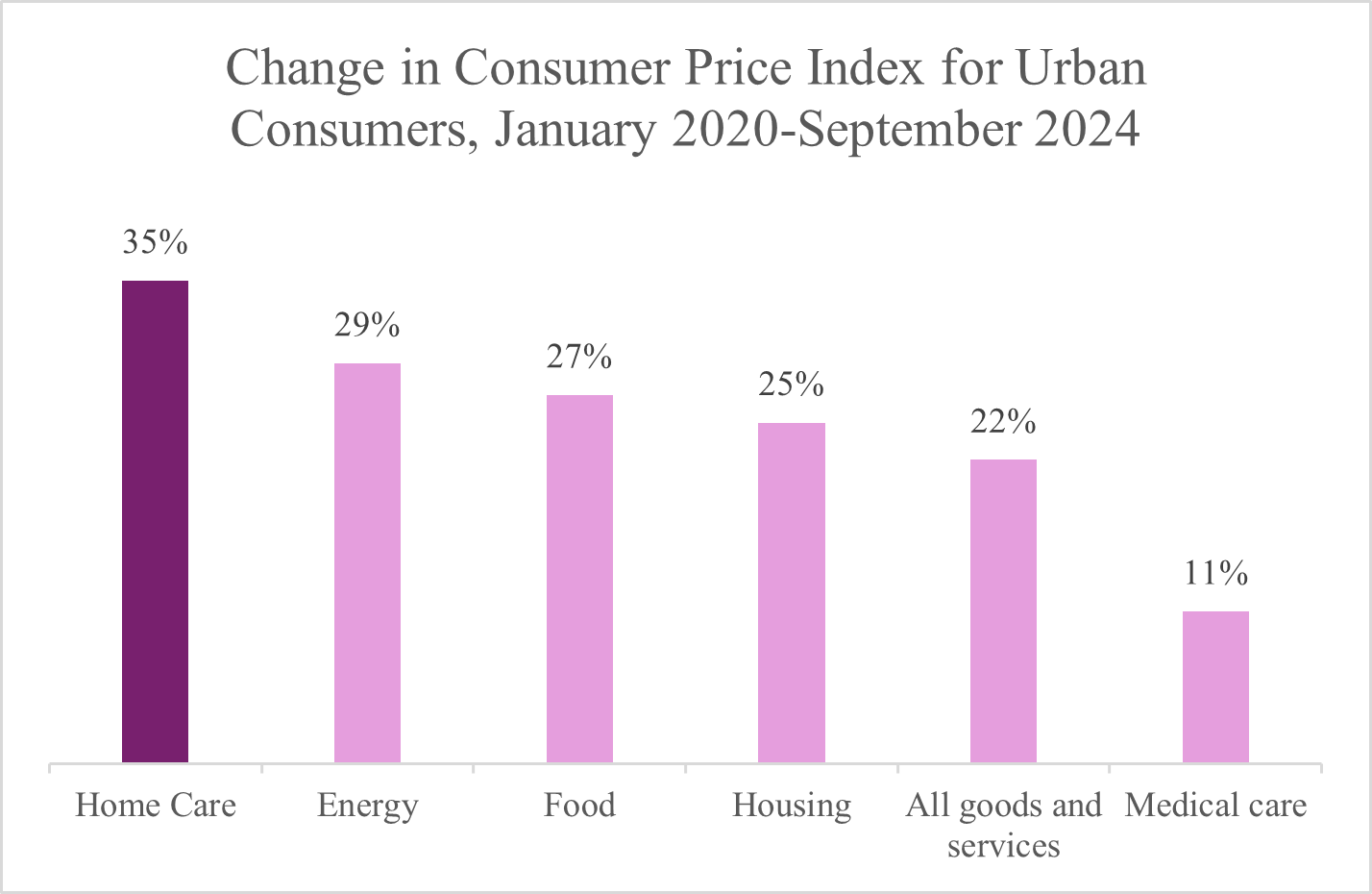

Home care inflation outpaces general inflation and most major categories

Indicative of the severity of the issue is how home care costs have skyrocketed compared to just before the beginning of the COVID-19 pandemic—and at an even greater clip than general inflation. Between January 2020 and September 2024, the price index for home care rose by more than one-third (35%). In other words, money that in recent years could have paid for 12 hours of home care now may not even cover eight hours. By comparison, general inflation over the same period was slower at 22%, as were categories commonly associated with high inflation in recent years such as energy (29%), food (27%), housing (25%), and medical care (11%).

Price increases took place more recently than the 2022 inflation spike

The trend of high inflation in home care is all the more relevant at the moment since inflation in other categories has slowed. General inflation soared in 2022, driven in no small part by increases in food, housing, and energy costs. Around that same time, home care inflation remained relatively low, increasing on average just 4% from 2021 to 2022. Since then, prices for home care have only continued to rise and in recent months have done so at an unprecedented rate. In every month of 2023 and so far in 2024, home care inflation has outpaced general inflation and inflation for most major categories.

The starkest example is March 2024, which saw home care prices increase by more than 14% relative to March 2023. General inflation for the same period was close to 4%, with other major categories at that same level or lower. The first half of 2024 saw home care prices increase by 11% compared to the first half of 2023. While prices seem to have cooled in the most recent months, costs remain unsustainably high for most older adults.

Consumers and family caregivers directly feel these price increases. According to Genworth, the median annual cost for home care (40 hours per week) was $68,640 in 2023. Of note, Genworth estimates that home care costs increased by 10% between 2022 and 2023, which is consistent with the federal inflation data. The high cost of home care is particularly difficult for older adults given their strong preference for remaining in their communities and their residencies for as long as possible.

Older adults and families need support to better afford paid care

Just as inflation increases pressures on most household budgets, home care inflation places unique strain on older adults and family caregivers.

More expensive prices for home care make these important services less accessible to the average older adult. Going without this support can create dangerous situations and leave an individual at greater risk of falls and other events that could jeopardize their health and safety. At the same time, rapid price increases can quickly deplete the average older adult’s household financial resources, reducing their ability to pay for other expenses, increasing stress, and reducing their quality of life.

Rising costs for LTSS also exacerbate another challenge. Already, family caregivers spend a large portion of their incomes on caregiving-related costs, and collectively provide unpaid care valued at an estimated $600 billion. That means LTSS cost increases put even more pressure on family caregivers, either in the form of providing financial support to people for whom they care, or providing additional unpaid caregiving in the face of rising costs for paid care — or both.

Policy and practice can help address LTSS affordability over the long term. Increasing the supply of direct care workers would help limit further cost increases, as workforce shortages are likely a main cause of price increases. In addition, another protection against runaway cost increases would be to ensure a robust market of LTSS options, including home care services, models of assisted living designed to be affordable for middle-class budgets, as well as scaling generally less expensive community-based options like adult day services and Programs of All-Inclusive Care for the Elderly. Increasing short-term supports that can delay long-term care, such as restorative programs like CAPABLE, can help stave off high cost services. And of course, supports for family caregivers such as paid leave, tax credits, and easily accessible respite care can help reduce strain for this group.

The need for solutions

LTSS financing today is arranged such that very wealthy households can afford expensive care and those with little or no financial resources can qualify for Medicaid. This leaves most people paying for care out-of-pocket and vulnerable to price increases and rapid home care inflation. In the absence of public financing at a broad scale, making LTSS affordable for older adults and family caregivers will require creative thinking at all policy levels — federal, state, and local — as well as private sector solutions, to ensure people can afford the care they need.

Search AARP Blogs

Recent Posts