AARP Hearing Center

State Health Insurance Waivers: Increasing Interest, Immense Implications

By Olivia Dean, Jane E. Sung , September 10, 2019 11:32 AM

In light of continued interest around the Affordable Care Act (ACA), it’s important to remember that the ACA includes a mechanism for states to make significant changes to parts of the ACA. While there are limits, states can use Section 1332 State Innovation Waivers (named after the section of the ACA that created them) to waive and alter certain provisions of the law.

In the past few weeks alone, several states have had State Innovation Waivers approved. As other states consider or actively pursue waivers, our new report provides a guide for states to understand the landscape and history of these waivers and how they can impact older adults. Among the topics discussed: recent federal guidance on the waivers that has raised questions concerning its implications.

The ACA’s Intention

In theory, State Innovation Waivers can be a way to improve the law. They were authorized in the ACA to allow states to innovate and can help states increase stability in their health insurance markets. But what’s key are guardrails in the law to ensure states don’t use waivers to undermine important ACA protections. States must prove that coverage provided under a waiver will be at least as comprehensive and affordable and will cover at least as many people as coverage without the waiver – without costing the federal government more.

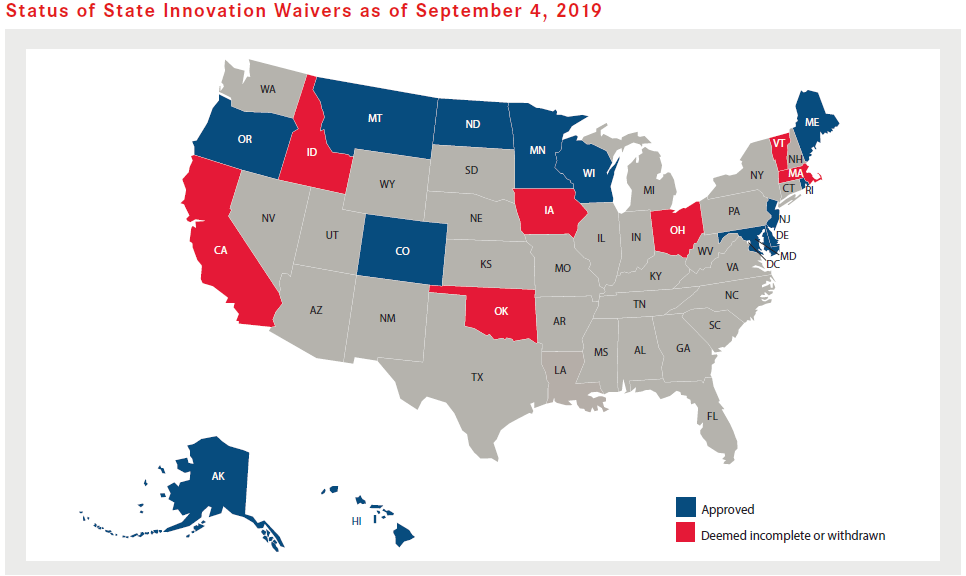

Thus far, the waivers have proven productive. States have mainly used them to create state reinsurance funds to help stabilize their markets. Thirteen states have had waivers approved to date, and twelve created state reinsurance funds. Reinsurance protects insurers from the uncertainty of high health care claims, which allows insurers to set lower premiums for consumers. This helps stabilize health insurance markets. Several of these reinsurance programs have already proven to help lower premiums, increase consumer enrollment, and maintain insurer participation.

New Guidance, New Questions

The federal government released guidance last year with a very different interpretation of State Innovation Waiver requirements than previous guidance. Unfortunately, the latest guidance relaxes the law’s requirements, including by allowing certain plans[i] that do not comply with the ACA to be considered acceptable coverage – and even allowing subsidies to be used for such plans. In a departure from previous guidance, waivers can now be approved even if they have a negative impact on vulnerable populations like older Americans.

A Situation to Monitor

It’s important to keep an eye on waivers that could be drafted in the coming months and years under the recent federal guidance, as well as any other federal changes to waiver authority.

State Innovation Waivers give states flexibility to be innovative and can improve health insurance markets and lower costs, but they could also have a negative impact for older adults if used the wrong way. It’s critical that federal and state policymakers uphold the ACA’s core guarantee of access to affordable, comprehensive health coverage for consumers, including older adults and other vulnerable groups.

[i] Including short-term limited duration insurance (STLDI) and association health plans (AHP).

For more on this issue, check out our latest Insight on the Issues on State Innovation Waivers and our previous Spotlight on the waiver guidance.

Olivia Dean is a policy research senior analyst at the AARP Public Policy Institute. Her areas of expertise include public health, health disparities, private health insurance coverage, and emerging health trends.

Jane Sung is a senior strategic policy advisor at the AARP Public Policy Institute. Her areas of expertise include health insurance coverage, including private health insurance market reforms, Medicare Advantage, Medigap, and employer and retiree health.

Search AARP Blogs

Recent Posts